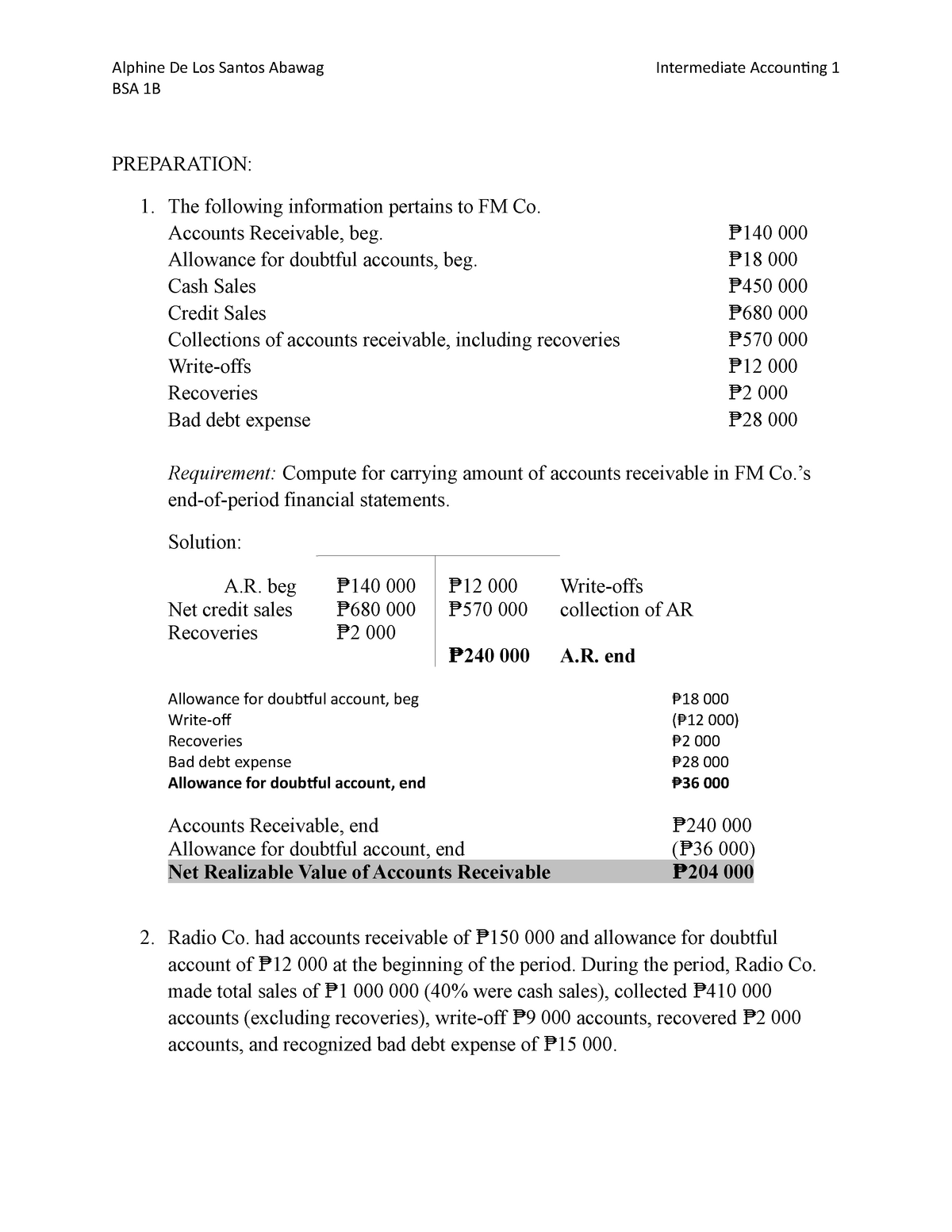

Simply how much would you borrow buying a home from inside the 2024? As the charges for the typical home improve, mortgage limits will follow fit. Here, i break down the modern restrictions having antique, FHA, and you may Virtual assistant and exacltly what the limit home speed might be created towards simple down payments (3%, 5%, 10%, & 20%).

2024 Va financing limit: $766,550

We secured primarily conforming mortgage loans significantly more than. A conforming financing is considered the most well-known variety of home loan to have a frequent homebuyer. They suits the rules lay because of the bodies-paid enterprises (GSEs) such as for instance Federal national mortgage association and you will Freddie Mac computer. These pointers are criteria for example loan amount, borrower’s creditworthiness, together with loan-to-value ratio. What goes on if you would like obtain more than new conforming loan restrict? You might consider a great jumbo financing. A great jumbo mortgage was an interest rate you to exceeds installment loans online Idaho bad credit brand new compliant financing limit. Jumbo funds are often utilized by homebuyers to acquire highest-well worth properties during the pricey areas or the individuals seeking money deluxe house. They provide individuals on the opportunity to financing services one surpass the fresh restrictions out of compliant fund, however they also come which have stricter qualification requirements and higher can cost you.Going for between a conforming financing and you may good jumbo loan utilizes some issues as well as your finances, the cost of the house or property you have in mind to order, plus enough time-name economic needs. Here are some reasons why you could potentially like a compliant mortgage more than a good jumbo mortgage:

- Mortgage Restrictions: Compliant finance conform to particular mortgage limitations set by Government Houses Financing Agency (FHFA), which can be modified a year considering alterations in casing costs. If for example the cost of the home you’re interested in drops contained in this the newest compliant mortgage limitations towards you, opting for a conforming mortgage is generally far more advantageous whilst generally speaking boasts straight down interest levels and a lot more favorable conditions.

- Straight down Rates of interest: Compliant money tend to incorporate lower rates of interest compared to jumbo funds. For the reason that conforming loans are believed safer to have lenders as they follow the principles lay of the government-paid people such as Federal national mortgage association and you can Freddie Mac.

- Much easier Qualification: Conforming financing normally have even more lenient qualification standards compared to the jumbo financing. Thus borrowers may find it easier to be eligible for a compliant loan in terms of credit history, debt-to-income proportion, or other activities.

- Supply of Home loan Activities: Compliant finance bring some mortgage points and additionally fixed-rates mortgage loans, adjustable-rates mortgages (ARMs), and you will government-covered financing instance FHA and you can Va funds. These solutions give consumers having self-reliance to choose financing device you to most closely fits their demands.

- Lower down Fee Possibilities: Compliant finance have a tendency to give reduce fee choice compared to the jumbo fund. Some conforming funds create borrowers to put down only 3% of the residence’s price, and then make homeownership much more available to a wider selection of consumers.

Alternatively, you can like good jumbo loan if for example the possessions you are curious inside is higher than the conforming loan constraints near you, or you favor a specific sorts of financial equipment otherwise words which might be limited with jumbo loans. Likewise, if you have a robust economic reputation and can spend the money for higher down payment and you will more strict qualification standards with the jumbo fund, it could be a practical option for your.

At some point, it is critical to carefully consider your debts and you can a lot of time-label requirements whenever deciding ranging from a compliant loan and you can a great jumbo financing, also to consult with a home loan elite to explore the choices.

Does this suggest no one can get a mortgage for more than $766,550? No. The conforming loan limit ‘s the restriction amount that can easily be secured because of the Federal national mortgage association and Freddie Mac computer (the government-paid organizations otherwise GSEs). One guarantee have professionals with regards to the mortgage recognition process and you will interest rates. There are numerous mortgage choices for highest numbers or you to definitely are not protected by the GSEs, however, conforming money account fully for an enormous most of the brand new mortgages.

$766,550 is the foot count. More expensive components gain access to higher limitations in line with the average home prices because town. The new county from the state constraints was indexed separately, Right here. The greatest level is $step 1,149,825 (foot financing limit x step one.5).

This new Federal Property Money Department (FHFA) is the regulator of your GSEs. It publishes certain home rate analysis. Due to the fact information is in for the next quarter (generally by the later November), it is compared to the third one-fourth of previous year and you may home prices is modified by the associated count.

In instances where home prices fall, the fresh limit doesn’t slide, however it doesn’t go up once again until home values flow back above the membership with the earlier restriction. Including, let’s say the mortgage maximum are $700k, however, pricing decrease enough to shed they so you’re able to $600k. The latest restrict create stay at $700k year after year (in the event pricing was in fact rising) until prices returned more than $700k.

All of that being told you, even with brand new , year-over-12 months amounts stay in confident area. Another graph includes your situation Shiller HPI and therefore concentrates on the fresh new 20 biggest urban area portion (it’s not employed for compliant mortgage limitation calculation, it as well is within sparingly confident region year more season).

2024 FHA financing restriction: $557,750

Perhaps “sparingly confident” wrong title. Whatsoever, yearly domestic speed fancy of five.5% Far is preferable to the newest Fed’s dos% inflation targetbined to your large rates within the age a little more 1 month before, this speaks into the previously-present value condition.

Conforming financing constraints can play some small part in aiding affordability into the the total amount that somebody means a beneficial $766,550 home loan and are struggling to get/refi toward previous maximum regarding $726,2 hundred.

The brand new limitations enter into feeling getting finance acquired by the GSEs in 2023. One generally speaking setting loan providers can use the brand new limitations immediately whilst requires at the very least thirty days to have yet another mortgage becoming ‘delivered’ towards the GSEs. Lenders commonly embrace the fresh new constraints in the a bit more paces.

Commander loan providers will mention all of them today. Laggards takes a couple weeks. Many lenders preemptively considering restrictions out of $750k, knowing that the real limitation is at the least you to highest and that it wouldn’t need to send those people loans in order to new GSEs up until 2024.

What about FHA financing limits? They have yet , to-be launched. This past year it just happened on the same big date once the FHFA. In any event, the brand new formula is well known. FHA will be 65% of FHFA Compliant Mortgage Restriction otherwise $498,250 (circular out-of a calculated worth of $498,).